RoSCTL Scheme (The Rebate of State and Central Taxes and Levies)

An Overview

The cabinet of India approved the RoSCTL Scheme to rebate all state and central taxes for garments and made-ups by replacing the previous scheme Rebate of State Levies, which provides only rebates of state taxes. The RoSCTL Scheme came into effect from 07/03/2019.

As we know, the USA has filed a complaint against India at the World Trade Organization (WTO). The complaint is that the Indian government gives undue benefits to Indian Exporter under export subsidies like the MEIS scheme, and it is against the WTO rules. Therefore, the Rebate of State and Central Taxes and Levies (RoSCTL) Scheme is a new scheme introduced by the Ministry of Commerce. Currently, RoSCTL scheme is only valid for garments and made-ups (i.e., Chapter 61, 62 & 63). Further, this scheme would be extended to all sectors.

As per Public Notice No. 58/2015-20 Dated 29.01.2020, Merchandise Exports from India Scheme (MEIS) has also been withdrawn for Export items falling under Chapter- 61, 62 & 63, w.e.f, 07.03.2019.

Rebates under the RoSCTL scheme

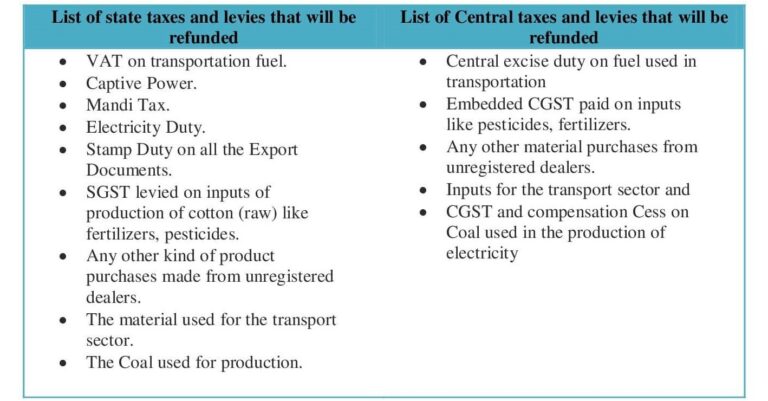

The RoSCTL Scheme gives rebate of the state and central taxes. Please find below list of state taxes and levies that will be refunded along with a List of central taxes and levies that will be refunded under the RoSCTL scheme DGFT.

RoSCTL Scheme Rates

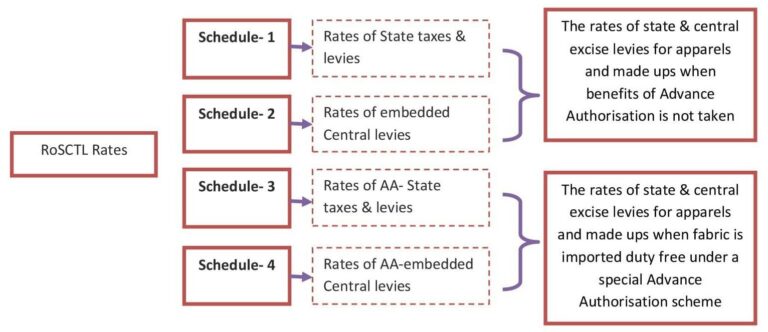

As per Notification No. 14/26/2016-IT (Vol.II) dated 07.03.2019, the RoSCTL rates have been notified as schedule 1, 2, 3 & 4 as follows:-

Schedule 1 & 2 - The rates of state & central excise Levies for apparels and made-ups.

Schedule 3 & 4 - The State & central excise Levies rates for apparels export when the fabric is imported duty-free under a special Advance authorization scheme.

The RoSCTL Rates are given as follows:-

What is additional ad-hoc Incentive under RoSCTL Scheme DGFT?

The Ministry of textile (MoT) has announced an additional AD-HOC Incentive of 1% on Free-On-board Value (FOB).

The additional Adhoc Incentive is calculated by the difference between new rebate on State and central taxes and levies scheme and the old rebate on State levies (RoSL) and Merchandise Exports from India Scheme (MEIS).

The additional incentive upto 1% is given only when the benefits received in RoSCTL is lesser than the combine benefit received in RoSL and MEIS. The Benefit is calculated on FOB value of shipping bill.

The period to claim the additional Adhoc Incentive is from 07th march 2019 to 31st December 2019.

How is the benefit given under the RoSCTL scheme?

Previously under the Rebate of State Levies (RoSL) scheme, the Rebate was directly credited into the Exporter bank account as notified by the Ministry of textiles same as Duty Drawback.

However, the benefit under the new RoSCTL scheme along with additional ad-hoc incentive is given in the form of duty credit scrips same as MEIS scrips. The RoSCTL scrips will be freely transferable in nature.

Just Like MEIS scrips, RoSCTL licenses can be used for payment of Import duties or can be sold in the open market at a premium rate.

Documents required to apply for RoSCTL Scheme

Below documents are required, to process the online application for RoSCTL scheme:

- Shipping Bill Copy

- DGFT Digital Signature

- Valid RCMC (Registration Cum Membership Certificate)

While applying online application, the Applicant has to make separate online applications for:

- S.B’s having Let export date between 7th March 2019 and 31st December 2019

- S.B’s having Let export date after 1st January 2020 Till 31st March 2020

As per new Public Notice No. 58/ 2015-2020 DT. 29.01.2020, please Note the Last Date of filing of an application for Duty Scrips under RoSCTL scheme will be:

- For shipping bills with Let export date between 7th March 2019 and 31st December 2019, the last date of filling online application is 30.06.2020.

- For shipping bills with Let export date from 1st January 2020 till 31st March 2020, the last date for filing an online application will be within one year from the date of Let Export Date.

Procedure to apply for RoSCTL scheme:

The RoSCTL Scheme came into effect on 7th March 2019. To claim the benefits application shall be done on the DGFT Portal of the shipping bills till 31st December 2021.

As per the latest advisory from the Government various changes have been done in the system to implement the RoSCTL scheme w.e.f. 1st October 2021.

Procedure to avail the benefits from DGFT

- The Applicant has to fill an online application using a digital signature.

- Linking of E-BRC’s is not required for applying the RoSCTL application.

- 50 shipping bills would be allowed in 1 application.

- As per Para, 3.09 (HBP) Facility of split scrips is available.

- The Applicant can choose the port of registration for EDI ports from where export is made.

- Separate applications to be made for EDI and non EDI ports.

- If the Applicant is under DEL (Denied Entities List) list, he/she can’t make an application.

- The Applicant can apply within one year from the date of uploading of the shipping bills from ICE Gate to DGFT server. Any application filed beyond this period would be time-barred as no late cut provisions are applicable.

- RoSCTL Licenses will be valid for 24 months from the date of issue.

Procedure to avail the benefits from ICE Gate Portal

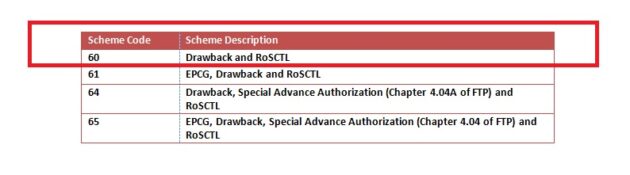

To avail of the benefits under the RoSCTL Scheme, the claim has to be made by the exporter in the EDI shipping bill by using specific scheme codes.

The options for the RoSCTL scheme are being provided with separate scheme-code as listed below -

Scheme code under RoDTEP Scheme

- In the absence of proper scheme codes, the RoSCTL benefit would not be available.

- Scroll would be generated by the custom after filing the EGM.

- Application shall be done to get the scrip on the ICEGate portal after generation of the scroll.

Some Important Points to note about RoSCTL scheme

- The rebate under the RoSCTL scheme is allowed subject to the condition that foreign remittance for the shipment made will be realized in stipulated time frame as per FEMA.

- If the sales proceeds are not realized within time allowed, then all the RoSCTL scheme benefits must be returned with 15% annual interest.

- All the original export documents along with shipping bills are required to be maintained by the exporter for a period of 3 years from the date of issuance of RoSCTL scrips.

- If the applicant fails to submit all the original documents asked by the licensing authority, then he/she will be liable to return entire benefit with applicable interest.

How can we assist you in claiming benefits under the RoSCTL scheme?

We assist our clients in the preparation of documents in providing hassle-free services.

- Prepare and submit online applications to obtain the License under the RoSCTL scheme.

- Registration of the License done in custom from our office.

- We also assist in the selling of licenses, provide help in documentation for the transfer of a license to the buyer.

- Also, do the online transfer by recording the details on the DGFT website.

- Consult our clients about the benefits they can avail of on their products and the country in which they export.